RiskSim: a system designed to produce returns while controlling risk

One of the core strengths of RiskSim is the insight that it provides into the potential drawdowns that a portfolio can face. The origins of the name come from the risk assessments that were generated using montecarlo simulation incorporating numerous "volatility environments" and "correlation structures". There are a number of different methodologies that are used to provide useful estimates for various activities from macro trading to high yield to distressed.

Scenario Shock Analysis

A proprietary method that uses ordinal ranks for securities to estimate ex-ante volatility. This method is particularly useful for securities with no data, where the historical data is no longer relevant, or where the historical data is statistically ill-behaved.

Scenario Horizon Analysis

The horizon analysis uses the estimated volatility of a state variable (price, spread, rates) to project the movement of the underlying security and reprices the security on the horizon date. This method is useful for securities where volatility surfaces can be estimated using options or where we feel comfortable specifying the volatility for a scenario.

Carry Analysis

It is useful to have an estimate of "true" carry since carry can absorb adverse price movements over a given horizon. The RiskSim carry analysis is parameterized to exclude price amortization and/or inkind carry under certain conditions. For example, distressed securities generally trade to a (non-par) recovery or restructuring value, so including par-based price amortization would be misleading.

Liqudity Analysis

Properly measuring portfolio liquidity is a critical componenet of effective risk management. The RiskSim approach includes ordinal ranking for each security, transition matrices to monitor the evolution of portfolio liquidity, and measures of liquidity provided by hedges, monitoring implicit as well as explicity leverage, etc.

Stress Indicators

Risk management in stressed or systemic environments is very different than risk management in "normal" environments. RiskSim has a proprietary methodology to aid in monitoring the risk of transitioning to a stressed environment. Many people track indicators which are more symptom than cause. The RiskSim indicators are the most reliable root indicators.

Portfolio Attribution

RiskSim has a unique approach to portfolio attribution that is useful for total-return portfolios. The approach uses a hiearchical mapping of benchmarks and, at each level, compares the return of the portfolio securities to the return that would have been generated by investing in the benchmarks. This approach properly accounts for intra-period trading to make this approach a true multi-period attribution approach. This approach is colloquially called the "this-instead-of-that" approach because it answers the question of what the return would have been if the investment had been made in the benchmark ("that") instead of the security ("this").

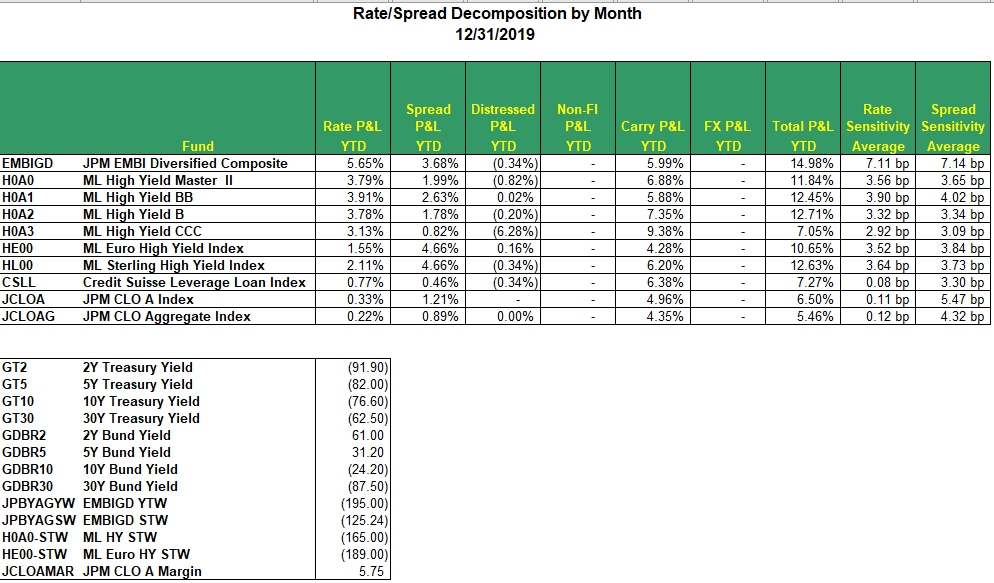

Rate-Spread Decomposition

The P&L of a portfolio is decomposed into Rate P&L, Spread P&L, Distressed P&L, Non-Fixed Income P&L, Carry P&L, and FX P&L. The Rate Sensitivity and Spread Sensitivity can be used to tie out to movements in rate and spread benchmarks.

Sample output for some popular fixed income indices. The columns would expand to show results by month.

Click to zoom!

Index Constituent Analysis

Many portfolios are regularly compared to a benchmark index. For example, high yield funds are usually compared to the ML High Yield Index. RiskSim can perform any analysis on any index for which the constituent data is available. For example, the Rate-Spread Decomposition can identify the precise source of the differences in returns between the portfolio and an index.

Volatility Simulation

The reason that the realized distribution of many asset prices have fat tails, particularly for high frequencies, is that volatility is not constant. RiskSim has a number of methods for simulating this behavior by getting volatility scenarios using partitioned historical data or by specifying the distribution of volatility. In addition, correlations are notoriously unstable. Combining volatility scenarios with correlation scenarios and sampling from those combinations yields a rich set of outcomes that can be used to produce a more realistic set of portfolio outcomes than using a single parameterization of the risk space.

Portfolio Volatility/Tracking Error

RiskSim uses duration-adjusted proxy mapping to generate estimates of portfolio volatility. If there are well defined sub-indices, RiskSim can estimate the tracking error.